NAMA ORGANISATION AND SERVICE PROVIDERS

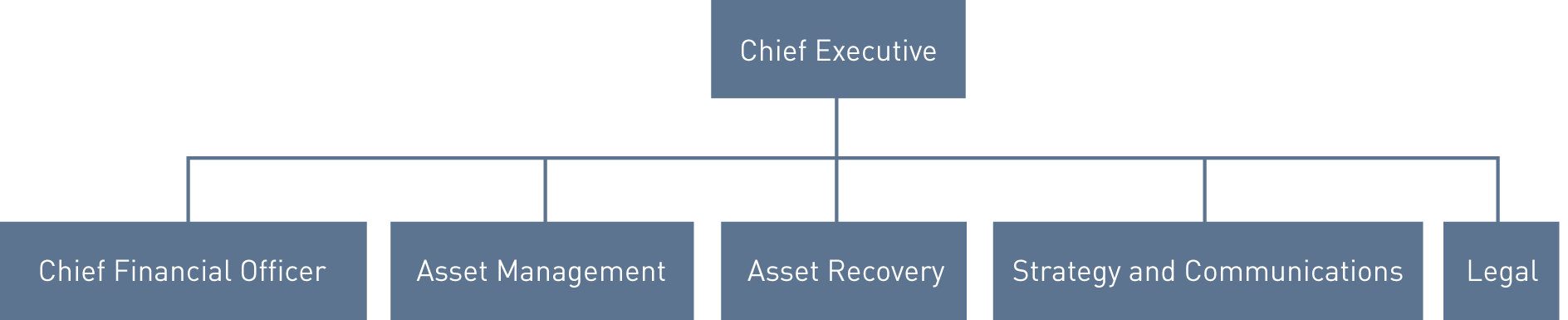

ORGANISATIONAL STRUCTURE

During 2012, NAMA marked its evolution from its establishment and loan acquisition phase to a new phase during which it focused on developing and implementing strategies aimed at extracting maximum recovery from its assets over medium- and long-term horizons. In late 2011, the Board approved a revised organisation structure designed to respond effectively and dynamically to the challenges ahead. The reorganisation, which was implemented in April 2012, involved the restructuring of the Agency into five divisions:

| FIGURE S: NAMA structure |

|---|

|

STAFF RESOURCES

The number of NTMA staff assigned to NAMA was 224 at the end of 2012. By the time recruitment has been completed for management of the original NAMA portfolio (that acquired under the Act), staff numbers are expected to be as follows:

| Division | Projected4 |

|---|---|

| CEO / Senior Executives | 6 |

| Asset Management | 16 |

| Asset Recovery | 153 |

| Chief Financial Officer | 57 |

| Legal | 32 |

| Strategy and Communications | 10 |

| Total | 274 |

35 members of staff have resigned since the inception of NAMA, including 25 resignations during 2012.

Acquisition of loans from the IBRC portfolio later in 2013 will give rise to additional staffing requirements within NAMA but it is not yet possible to be more specific until there is greater clarity about the volume of loans to be acquired from the Special Liquidators.

ASSET RECOVERY

The Asset Recovery division, which comprises 153 staff, has three primary functions: strategy delivery, management of debtors/receivers and maximising cashflow while minimising loss.

Asset Recovery is the principal interface with debtors/receivers and is responsible for over 99% of the debtor connections, both directly managed by NAMA and indirectly managed through the PIs. This responsibility requires intensive daily management with an innovative and solutions-based approach employing a range of work-out methods including the following:

- Setting and actively monitoring clear strategies, targets and milestones;

- Minimising debtor and receiver costs;

- Securing and maximising income;

- Optimising sales values through proactive asset management;

- Providing additional capital expenditure where additional value can be obtained or value protected;

- Employing vendor finance and loan sales where appropriate;

- Reviewing, on a regular basis, asset sale versus asset hold options, using discounted cash flow analysis.

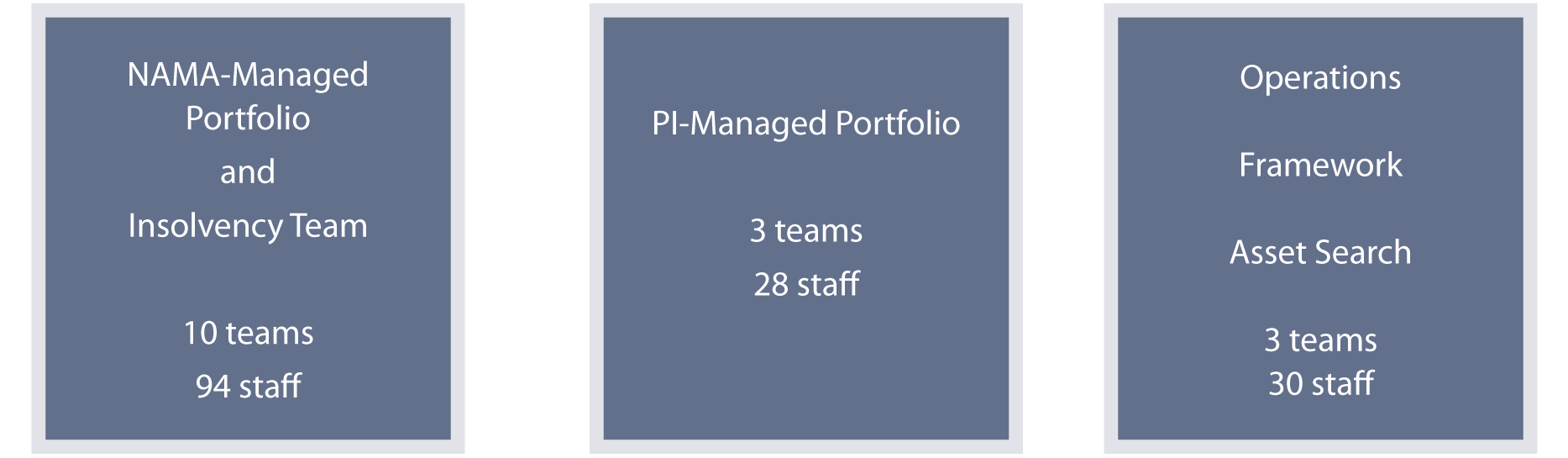

The Division is structured as follows:

| FIGURE T: Structure of Asset Recovery Division |

|---|

|

| DEBTOR CASH FLOWS |

|---|

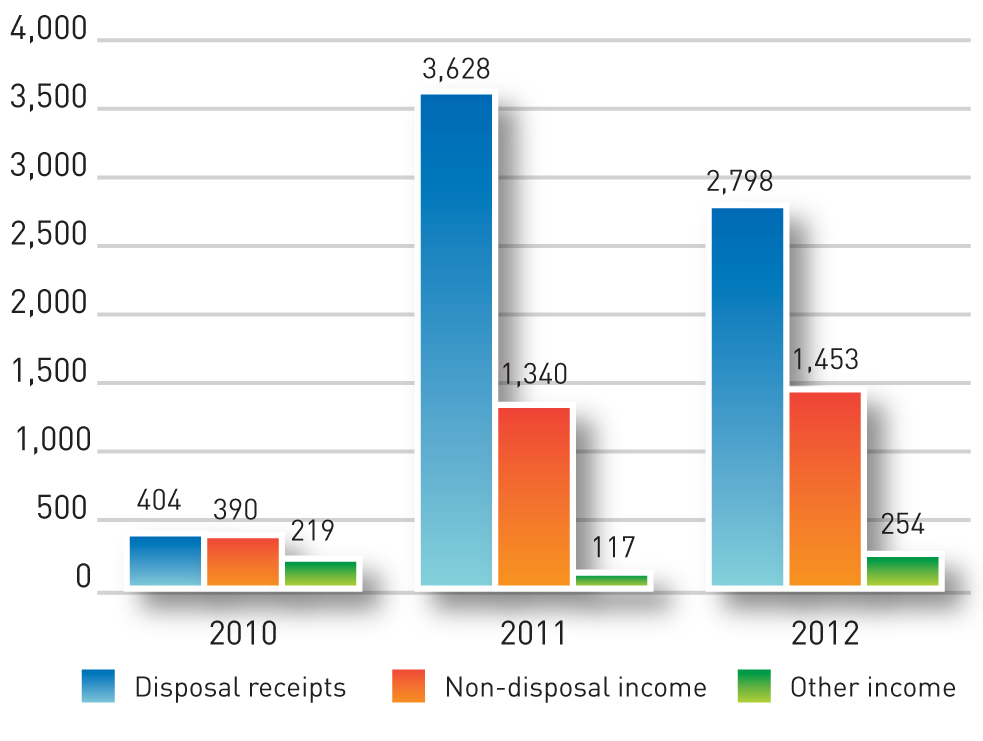

| The Asset Recovery division is primarily responsible for direct engagement with debtors and for optimising the cashflows generated by debtor assets so as to enable key debt repayment targets to be met. Figure U below presents annual aggregate cashflows arising from disposal proceeds and other (mainly rental) income from 2010 to end-2012: |

| FIGURE U: Receipts from debtors - 2010-2012 |

|

NAMA-MANAGED PORTFOLIO

The NAMA-managed portfolio includes 189 debtor connections with original par debt of €61 billion. All but three5 of these debtor connections are managed by nine multidisciplinary Asset Recovery teams of nine/ten staff per team which engage directly with debtors in relation to business plans, credit applications and monitoring of targets and performance. By June 2012, the review of the business plans of some 775 debtor connections had been completed (400 directly reviewed in NAMA and 375 reviewed jointly with the PIs). Invariably, the business plan process gave rise to difficult and intensive negotiations on contentious issues (for example, Principal Dwelling House ('PDH'), early asset sales, reduction of overheads, asset reversals and securing charges over otherwise unencumbered assets).

PI-MANAGED PORTFOLIO

The PI-managed portfolio includes 586 debtor connections with €13 billion of original par debt. Table 14 below provides a breakdown of the PI-managed debt by reference to the three PIs which were managing the portfolio at the end of 2012.

| AIB | BOI | IBRC | Total | |

|---|---|---|---|---|

| Debtor Connections | 222 | 59 | 305 | 586 |

| Par Debt (€ billion) | 5.3 | 2.0 | 5.1 | 12.4 |

| NAMA Debt (€ billion) | 1.7 | 1.1 | 1.3 | 4.1 |

On 7 February 2013, the Minister appointed Special Liquidators to IBRC. On 19 March 2013, NAMA announced its decision to move the management of the IBRC-managed portfolio on a phased basis to Capita. NAMA and Capita have begun the process of recruiting staff, largely from within the IBRC NAMA Unit, to carry out primary and special servicing on the portfolio previously managed by IBRC.

NAMA's enforcement activity is overseen by a team of specialist insolvency practitioners (based in the Asset Recovery division) in conjunction with the Legal division.

Both the NAMA-managed and PI-managed portfolios are supported by Asset Recovery Operations which includes Asset Search, Policy and Portfolio Operations teams.

To date, 58 debtor connections have been subjected to asset searches which have yielded additional assets valued at €7m.

ASSET MANAGEMENT

The Asset Management Division has a specific real estate and capital focus to identify and develop property assets with debtors, receivers and joint venture partners. The division aims to create and add value with the objective of enhancing cash flow, particularly over a medium-term horizon. In addressing this objective, it is focusing on a number of key development projects in Ireland and Britain which are considered to be commercially viable based on current or prospective demand and pricing. These projects, which are estimated to have a Gross Development Value in excess of €4 billion when completed, will be managed by the division through various stages of appraisal, planning, design and development.

After each phase in the development process, the Asset Management Division will subject developments to robust 'sell-hold' interrogation tests, with the intention of achieving the best return over the medium-term. This could involve the sale of the asset after a Local Area Plan ('LAP') has been finalised or after planning permission has been achieved or at any later point in the development cycle. The scope for Joint Ventures will also be assessed as a means of progressing projects.

Much of the division's activities in Ireland during 2012 was concentrated on planning issues. This involved extensive engagement with stakeholders in various projects, including owners/receivers and planning authorities. The division has engaged positively with various planning authorities on their LAP and SDZ processes and has also been active in obtaining new or amended planning permissions for specific sites.

Optimising the planning status of sites is a key prerequisite towards ensuring that NAMA can respond with agility to emerging demand for commercial and residential assets.

To date, much of the division's focus in terms of ongoing development projects has been on the UK, specifically the London residential market, where it is managing the active development of over 5,000 units. In Ireland, a number of projects have been identified which are intended to address prospective demand for office accommodation in central Dublin and for family housing accommodation also in parts of Dublin. For instance, as regards sites in the Dublin Docklands area over which it has security, NAMA has taken the lead in framing commercially viable proposals and in engaging from an early stage with the planning authorities and with potential investors and tenants. It is devoting considerable energy and resources towards determining the most appropriate solutions in terms of optimum development scale, mix, and timing of developments.

In addition to its asset management brief, the division also manages three significant debtor connections with aggregate par debt of €4 billion, principally secured by property located in Britain. In addition, it has taken a lead role in driving two NAMA initiatives, those relating to the provision of social housing and the Deferred Payment Initiative.

| ASSET MANAGEMENT - PROJECT SELECTION CONSIDERATIONS |

|---|

| NAMA will advance funds to enable the development of projects which it considers to be commercially viable, taking account of considerations of supply, demand and achievable sales prices. In the case of development proposals, some of the considerations which inform its project selection include the following: |

Through its engagement with the IDA and the four Dublin local authorities, NAMA has identified an emerging demand for new office accommodation within the Dublin Central Business District where leading global enterprises in the technology, business, financial and life sciences sectors are located and which is expected to remain the focus for continued strong FDI inflows over the medium-term. NAMA is also considering prospective demand for new commercial development across the country's major urban centres. In terms of residential development, NAMA recognises that there is a balance to be struck between current market demand for three-/four-bedroomed family houses in urban locations and the broad thrust of planning policy which seeks to encourage more sustainable development through the avoidance of excessive suburbanisation and the promotion of higher densities in appropriate locations. As a general principle, priority is given to sites in, or close to, established residential locations with existing supply constraints. |

The existing or achievable planning status of sites is an important consideration in project selection and therefore engagement with planning authorities on a project-by-project basis is crucial. NAMA also engages on a more strategic basis with the Department of the Environment, Community and Local Government, with the National Transport Authority and with planning authorities to discuss wider issues. The Agency is actively engaged, for instance, with all stakeholders including the Department of the Environment, Community and Local Government and Dublin City Council on the Draft SDZ Scheme for parts of the Docklands, which will replace existing Dublin Docklands Development Authority ('DDDA') Planning Schemes before the end of 2013. The SDZ is critically important in terms of the Agency's plans to support the development of new commercial office space in the city. In relation to residential housing, NAMA is engaged on policy matters such as residential density, infrastructure provision and potential future landbank requirements which need to be resolved at national, as well as at planning authority, level to underpin the delivery of residential development for which demand has been identified. |

The extent to which there is connectivity to existing services infrastructure, for example, drainage, water and electricity services, without disproportionate upfront capital expenditure, or delay, is an important consideration. |

Access to public transport services and road networks is an increasingly important consideration. Good transportation connectivity is a major consideration in terms of site selection. The existence of an established community and workforce and the availability of local amenities are central to the selection of commercial and residential projects. Local schools, convenience shopping and other social services are all important determinants of location choice. |

STRATEGY AND COMMUNICATIONS

The Strategy and Communications Division is responsible for strategic analysis of the portfolio and for developing strategies for NAMA on how best to attain its objective of obtaining the best achievable return. Its functions include regular formal review of NAMA strategy and the design and implementation of new products. The division also has responsibility for managing NAMA's communications activity, including the co-ordination of NAMA's engagement with the media, State agencies and with other key NAMA stakeholders.

The Strategic Planning team makes recommendations to Executive and Board as to the most appropriate strategies for NAMA to pursue in the context of its statutory objectives. The team prepares and analyses detailed portfolio data and analyses developments and trends in the market with a view to formulating appropriate recommendations. It monitors and reports performance on a number of key elements of NAMA Strategy.

It also has a role in new product development, including the design of the DPI and assessing the suitability of products such as Qualified Investor Fund ('QIF') and REITs. It is currently engaged with the ESRI in a research programme which will produce research reports on topics related to future supply and demand for residential housing in Ireland.

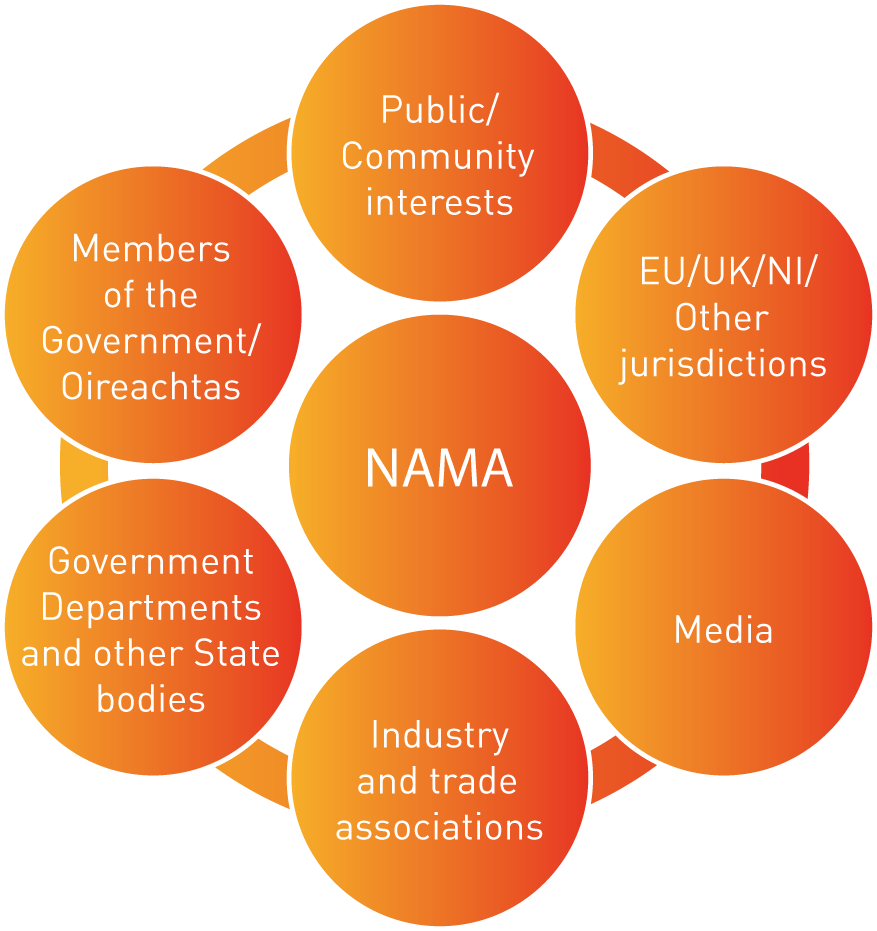

The NAMA Communications function is concerned with how best to communicate with stakeholders who have a legitimate interest in NAMA's activities to ensure that they are well informed about those activities and have a strong appreciation of the rationale behind initiatives undertaken by NAMA.

NAMA's principal engagement is with debtors and potential purchasers of assets controlled by its debtors and receivers and this engagement is conducted by the Asset Recovery and Asset Management teams. As the activities of NAMA debtors and receivers have an impact on the wider economy and society, there is a diverse range of other stakeholders (Figure V) with an interest in those activities and that creates a corresponding obligation on NAMA to ensure that its perspective is communicated to those stakeholders.

Given NAMA's scale and its potential impact on the Irish economy and society, public representatives, acting on behalf of their constituents, have a legitimate interest in NAMA's activities and NAMA, in turn, is keen to ensure that representatives are well informed about those activities, subject to commercial and banking law constraints. NAMA engages with public representatives through a number of channels including appearances by the Chairman, the Chief Executive and senior executives at Oireachtas committees. It also provides a dedicated email channel which enables Oireachtas members to raise particular issues of concern to their constituents, for example, unfinished estates, health and safety issues associated with derelict properties and other matters. A similar email channel is available to members of the Northern Ireland Assembly. NAMA also deals with issues of public concern through replies to Parliamentary Questions ('PQs') submitted to the Minister for Finance on NAMA matters (there were over 350 such PQs in 2012).

More generally, NAMA seeks to provide as much information to the public as is possible given constraints imposed by commercial imperatives and banking confidentiality law. This is partly done through normal channels such as press statements, speeches, responses to press queries, website updates and information leaflets on particular topics (example below).

NAMA also deals with a monthly average of about 150 email queries (through info@nama.ie) and an average of about 140 phone queries per month from members of the public.

| FIGURE V: Key NAMA stakeholders |

|---|

|

LEGAL

The Legal Division provides independent advice to the Board, the CEO and to NAMA business divisions on a range of legal issues that affect NAMA and its operations. It comprises a core team of over 30 legal professionals and support staff with expertise in commercial property, banking, insolvency and litigation. The Legal division played a key role in managing the extensive legal due diligence process required as part of the loan acquisition and valuation process.

The Division's role involves delivering legal solutions and managing legal risk in areas such as asset recovery, asset management, insolvency, operations, delivery of legal services by the participating institutions and on cross-functional Agency projects (for example, the DPI). The Division is directly involved in debt restructuring, lending operations, asset management strategies, enforcement and post-enforcement strategies and operations. To date, this has included providing strategic legal advice and identifying and managing legal risk on debt restructuring of more than €10 billion, asset and loan sales of €7 billion and enforcements of €3 billion.

The Legal Division provides legal advice and transactional services to Asset Recovery and Asset Management teams in respect of the NAMA-managed portfolio of 189 debtor connections. Following review of debtor business plans, Legal advises Asset Recovery and Asset Management on the implementation of NAMA's preferred strategy for the connection including all new project funding, supervision of asset sales, restructuring of loans and security, reversal of asset transfers and the taking of security over unencumbered assets.

The Legal Division provides advice and policy guidance to Asset Recovery in respect of the PI-managed portfolio which includes 586 debtor connections and provides direction and guidance to the legal teams in the PIs on legal issues arising on that portfolio. The Legal Division is also involved in documenting service standards and resolving service issues with the participating institutions.

The Division advises the Board and NAMA Group on legal issues, corporate governance and compliance obligations. Legal manages the governance structures of the NAMA SPVs and advises on NAMA's funding programmes.

The Division manages all litigation initiated or defended by NAMA, both in connection with its portfolio of loans and otherwise. During 2012, NAMA successfully dealt with a number of judicial review challenges. The value of judgements obtained in the Irish courts since inception is in excess of €1.1 billion.

The Legal Division advised on and implemented the legal structure for the DPI and has advised on the transactions necessary to deliver social housing units through outright purchase and also through the long term leasing model.

CHIEF FINANCIAL OFFICER

The Chief Financial Officer's areas of responsibility include Finance, Operations, Systems, Tax, Treasury and Audit and Risk.

The Finance team has responsibility for managing the organisation's financial and management reporting requirements. It comprises the following areas of responsibility:

- Preparation of Section 55 Quarterly Accounts and Annual Financial Statements.

- Liaison with external auditors regarding the year-end audit process.

- Monitoring and control of the organisation's operating costs.

- Management of the annual cost budget process and preparation of periodic updates.

- Advising on appropriate accounting, compliance and business administration considerations as part of new NAMA business initiatives (for example, the social housing initiative).

- Reporting of organisational key performance indicators ('KPIs') to Board, Board Committees and the Senior Executive Team.

- Preparation of management accounts and other key management information.

- Preparation of external presentations for key NAMA investors and stakeholders.

- Preparation of annual budgets and other forecasts.

- Management of the bi-annual impairment process.

- Preparation of Section 55 (the Act) Quarterly Report.

- Liaison with the PIs, Master Servicer and internal stakeholders regarding the delivery of loan data.

- Performance of key reconciliations of the loan data provided by the PIs/Master Servicer.

- Overseeing the recording of debtor transactions in both PI and NAMA systems.

- Maintenance and development of the NAMA Loans Warehouse ('NLW') system.

The Operations team has responsibility for:

- Oversight of the performance of the PIs as loan administration service providers to NAMA and of the NAMA Master Servicer.

During 2012, following the end of the debtor business plan review process, the full transition to direct NAMA management of larger debtors was achieved through the establishment of clear operational and case management protocols and re-engineering of processes with the PIs. - Oversight of various operational projects within NAMA. Key 2012 achievements included, inter alia, the establishment of a formal structure to mandate debtor rental income which is well advanced in terms of implementation and the implementation of the NAMA operational integration plan underpinning the 2011 merger of EBS and AIB.

The Systems team has responsibility for the design and specification, development and management of NAMA's IT systems.

A number of key systems milestones were achieved in 2012:

- The Portfolio Management System ('PMS'), which is NAMA's core property database and management tool, was fully implemented and rolled out in 2012.

- The Document Management System ('DMS') was also fully implemented in 2012. DMS acts as a repository for all documents.

- Significant enhancements were made to the NLW system, which acts as a central repository for all NAMA loan data and, in turn, feeds into other core NAMA systems.

- The Geographical Information System ('GIS'), which provides a geospatial visual of a specific property or properties, has been implemented and rolled out.

- The Argus software was implemented to support asset management decision-making and management of development projects.

Tax has responsibility for:

- Managing the organisation's tax compliance obligations.

- Designing, implementing and overseeing structures and protocols, both within NAMA and the PIs, to ensure that debtor/receiver taxation issues are appropriately considered as part of property and loan transactions.

- Advising on appropriate tax planning and structural considerations as part of new NAMA business initiatives (for example, Joint Ventures).

Treasury has responsibility for the management of NAMA's balance sheet risks and its liquidity requirements. Its main activities include:

- Management of NAMA's day-to-day funding and liquidity requirements.

- Balance Sheet asset and liability management ('ALM'), including management of currency and interest rate risks.

- Monitoring and forecasting NAMA's medium and long-term liquidity

- Management of NAMA's Debt Securities Issuance.

Audit and Risk has responsibility for:

- The design and implementation of the NAMA Risk Management Framework.

- Providing independent assessment of, and challenge to, the adequacy of the control environment and critical organisation processes (for example, impairment).

- Supporting the NAMA CFO to ensure that NAMA operates within Board-approved risk limits and tolerances.

- Coordination of the internal and external audit activities across NAMA, PIs and Master Servicer.

- Monitoring and reporting to the Audit Committee and Board on progress in addressing actions highlighted in audit findings.

- Oversight of NAMA's Quality Assurance function.