DEBTOR STRATEGIES

ACQUIRED LOANS

NAMA acquired more than 12,000 loans in a range of currencies which had been advanced to over 5,000 debtors (managed as 775 debtor connections by NAMA). The acquired loans were secured by more than 10,000 groups of properties across a range of asset classes and markets (these have now been further disaggregated into 56,000 saleable property units).

NAMA-MANAGED

The largest 189 debtor connections (generally those with par debt in excess of €75m) accounted for €61 billion of the par debt originally acquired by NAMA. Key credit decision-making and relationship management are carried out by NAMA while loan administration is carried out by the PIs.

PI-MANAGED

The other 586 debtor connections accounted for €13 billion of original par debt. Relationship management and loan administration are carried out by the PIs under delegated authority from NAMA. NAMA has a presence in each of the NAMA units within the institutions to oversee the management of the connections.

BUSINESS PLAN PROCESS

As part of NAMA's initial engagement with debtors, each debtor connection was required to undertake a comprehensive business plan process designed to assess its commercial viability and its willingness to co-operate with NAMA. The process required that debtors set out their debt repayment strategies, including their proposals for key property assets under their control. NAMA's insight into each debtor's position was informed also by the extensive legal and property due diligence which was provided as part of the valuation and loan transfer processes. Arising from this information, NAMA had a very comprehensive perspective on each debtor and was well placed to come to a realistic view as to a debtor's prospects of achieving ultimate commercial viability.

The engagement with debtors involved the assessment of 789 debtor business plans which was completed by end-June 2012 (a small number of connections prepared separate plans for different entities within the connection). Based on these assessments, strategies were adopted by NAMA towards each of the 775 debtor connections. Typically, debtor strategies tended to fall into three broad categories: (1) support, (2) disposal or (3) enforcement. Table 1 summarises the extent to which each strategy has been adopted to date.

| Strategy | % of NAMA debt |

|---|---|

| Support | 58% |

| Disposal | 18% |

| Enforcement | 24% |

| Total | 100% |

A disposal strategy is pursued where NAMA does not foresee a long-term engagement with the debtor concerned and, instead, focuses on working with the debtor in the implementation of a disposal strategy over a short-term horizon.

Set out below are more detailed accounts of what is entailed with the support strategy. For the enforcement strategy, click here.

SUPPORT

Support can take a number of forms, the most common of which is in the form of a letter of support which requires that a debtor implement a number of milestones in relation to debt reduction. The letter of support must be accepted by the debtor. Support may, in certain limited situations, take the form of a full or partial restructure of loans or may be provided without any changes to the underlying facilities. A full restructure involves the creation of a new loan agreement and associated security documentation. A partial restructure requires the operation of a Connection Management Agreement ('CMA') in conjunction with existing loan and security documentation. The CMA sets out the terms and conditions of business plan implementation and must be accepted by the debtor.

With NAMA support, debtors manage an agreed asset management and disposal strategy which will typically include some or all of the features outlined below.

| FEATURES OF DEBTOR SUPPORT |

|---|

Schedules of agreed asset sales with the timing of particular sales dependent on the type of property involved (for example, residential investment, commercial investment, land), the jurisdiction and location of the property and the scheduled expiry of any associated leases. |

Reversal of any transfers, which may have taken place over recent years, of assets to related parties (for example, spouses and other family members), including property, cash, shares and other gifts. |

NAMA's policy is to charge unencumbered assets as additional security, taking account of the transaction cost and any legal issues involved. Where another lender has security on a debtor's assets and in order to capture future upside potential, NAMA takes second charges over surplus equity where appropriate. |

Rental income from investment assets controlled by the debtor must be brought within NAMA's control. |

Where there is surplus cash available, it is netted against a debtor's loan obligations. Where appropriate, a debtor is required to sell shares, works of art and other non-property assets and apply such disposal proceeds against NAMA debt. |

In certain cases, NAMA provides funding which enables viable projects to be sustained and brought to completion with the view to increasing the long-term recoverable value of the assets. For further information, click here. |

OVERHEADS

NAMA seeks to ensure that income generated by assets securing its loans is applied towards repaying a debtor's indebtedness to the Agency. In certain circumstances, debtors are allowed to retain a portion of asset income to pay overheads, including staff costs, where this is necessary to preserve and enhance the value of underlying property security. Overhead costs fall into two broad categories:

- Costs associated with the repair and maintenance of properties, insurance premia, local authority rates and professional fees. These are essential costs which would be incurred regardless of whether the assets were being managed by debtors or receivers.

- Overhead costs also include an allowance for the debtor's approved salary and the salaries of staff employed by the debtor to manage the assets. The alternative in these cases is to appoint receivers whose costs tend to be higher than debtor and associated staff salary costs.

In agreeing to allowances for overheads, among the issues considered by NAMA are (a) the appropriate level of overhead given the complexity or otherwise of the debtor's business, (b) which, if any, members of the current management team are likely to add value if retained and (c) whether the management team needs to be strengthened or enhanced.

INCOME VISIBILITY

It became clear to NAMA, after its acquisition of loans, that there was significant and widespread leakage of funds - most notably rental income - which should properly have been applied by debtors towards debt repayment. NAMA set out to address this leakage as a major and urgent priority. Even prior to agreement of debtor strategies, NAMA required that debtors mandate rental income to secured bank accounts.

NAMA's approach involves oversight of the collection and lodgement of rental income. In cases where rents are substantial, it is a requirement that agents with a duty of care to NAMA be appointed by debtors to collect rents and to discharge associated property expenses. Rents are lodged to bank accounts over which NAMA has imposed security arrangements which preclude the release of funds.

In certain circumstances, particularly where NAMA has chosen to work with the debtor's management team, an annual budget for overhead costs and asset management expenditure is agreed and spending is then monitored on a periodic basis relative to budget. The approval and payment of legitimate asset management expenses from rental income and the ultimate application of residual rental income to service the outstanding debt is tightly controlled. This greater visibility and control of debtor cash flows has meant that rental income has become a significant and recurring source of revenue for NAMA with non-disposal cash inflows of the order of about €100m per month, notwithstanding cumulative asset disposals of €6.8 billion by end-2012.

FINANCIAL MONITORING

As part of its ongoing engagement with debtors, NAMA requires accurate and timely financial and management reporting from debtors, particularly in respect of the achievement of agreed milestones, debt repayment targets and current financial metrics such as rental receipts. Debtors are also required to provide future cash flow forecasts and other specific information requirements identified by NAMA case managers. In some instances, NAMA requires the appointment of independent monitors, including financial monitors, property management service providers and project managers, whose remit is to report to NAMA on the completeness and accuracy of information presented by debtors in relation to both historical and future financial and property management activity and agreed milestones.

ADDITIONAL SECURITY

To ensure that debtors repay their debt to the fullest extent possible, NAMA requires that they provide security over unencumbered assets not previously pledged as loan security and that they arrange for the reversal of recent asset transfers to relatives and others, where applicable. From inception to end-2012, NAMA had obtained charges over additional security with an aggregate value of approximately €642m and is in the process of taking security over additional assets identified in the course of its engagement with debtors. NAMA expects, after all negotiations with debtors have completed, that it will have obtained in excess of €750m as part of this process.

Additional security has been identified in a number of ways. NAMA's Asset Search team, for instance, is responsible for managing the implementation of asset searches designed to verify debtors' asset statements. In addition, NAMA case managers have identified debtor assets that may be available as additional security, including excess collateral identified through the valuation and business review processes and assets that fall within the scope of personal guarantees. Reversed asset transfers include transfers of cash, property assets, company shares and loans to family members.

Assets over which NAMA has obtained security under this programme include an Antiguan hotel (subsequently sold for about €19m), a New York office (sold for about €15m), a new office development in South Co. Dublin (sold for about €12m) and development land in the south east of England (sold for about €10m). In the case of another debtor, charges have been obtained over pensions, shares, art and antiques with an aggregate value of about €17m.

As part of the business plan process, a sworn statement of affairs was requested from personal debtors and guarantors, including details of any unencumbered assets which might be available to support repayment capacity and of any transfers of assets in recent years by debtors to relatives and associates. In completing that statement of affairs, debtors were reminded that the provision of false or inaccurate information to NAMA is a criminal offence, under Section 7 of the Act.

NAMA has referred two formal complaints to the Garda Bureau of Fraud Investigation arising from a possible failure by debtors to fully disclose their assets and liabilities in their statements of affairs to the Agency. NAMA has also initiated cases in the Irish and English High Courts and in the US and Canadian courts for the reversal of asset transfers, including residential property, shares and other assets.

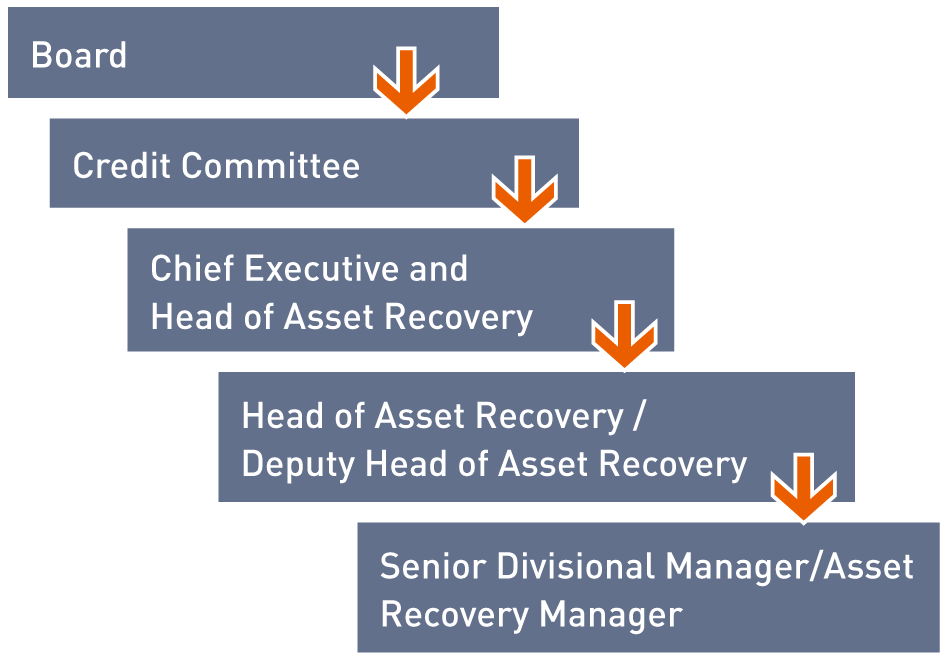

| NAMA CREDIT FRAMEWORK |

|---|

| NAMA's Credit Policy Framework sets out delegated authority levels for credit decisions, monitoring and reporting. Among the decision types covered by the Framework are approvals of Debtor Strategy Reviews, new lending, enforcement action, loan impairment, sales of assets and loans and asset management decisions. The level of approval required for each of these credit decisions is determined by reference to the size of the debtor's outstanding debt and the size of the proposed transaction. Credit decisions are approved by one or more of the following entities within a cascading level of approved delegated authority: |

|

| All credit decisions for loans managed by the PIs are approved by the PI's Credit Committee or by the requisite delegated authority within the institution (Head of Credit, Deputy Head of Credit or Senior Credit Manager). |

| Oversight of the compliance with Delegated Authority Policy is performed by the Quality Assurance team in NAMA. |

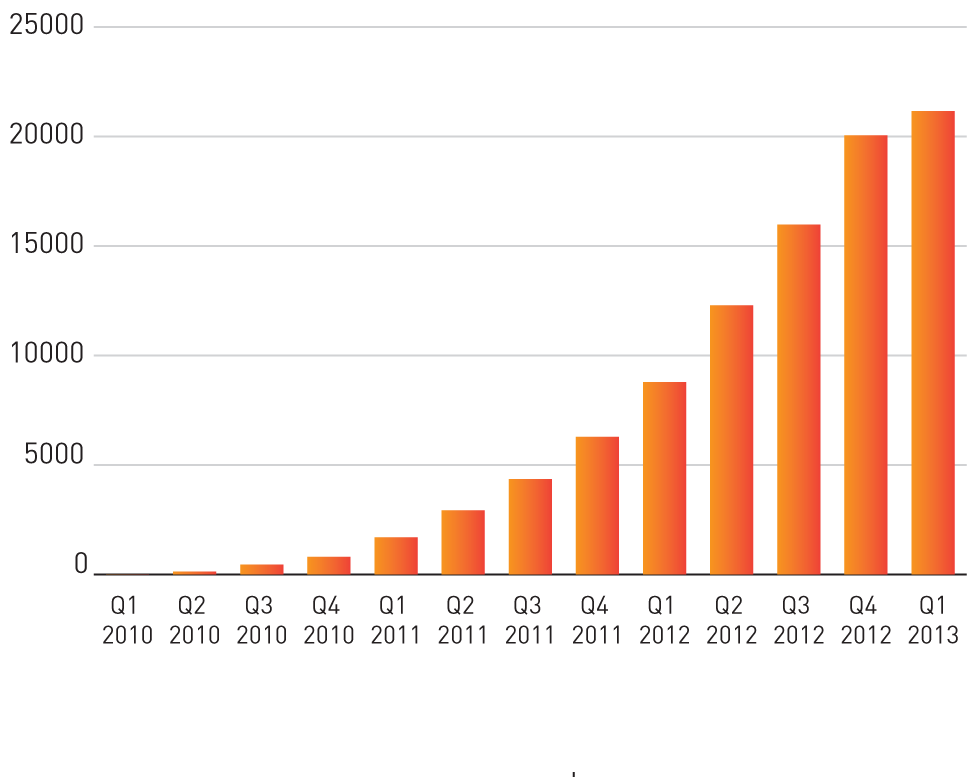

| From inception to end-2012, a total of 20,035 credit decisions were made, 13,749 of them in 2012. |

| FIGURE E: Credit decisions, cumulative since inception |

|

| The average turnaround time for credit decisions in 2012 was 5 days. |

DEBTOR CREDIT RATING

For NAMA-managed connections, NAMA operates a credit grading matrix across two dimensions – debtor performance and expectations of debt recovery.

Debtor performance incorporates NAMA's assessment of the extent to which set milestones have been met and the extent to which asset cash inflows are under NAMA control. It also incorporates progress on charging unencumbered assets (where applicable), on the reversal of asset transfers to connected parties (where applicable) and on cross collateralisation. Ratings are A (Satisfactory), B (Watch) and C (Enforced).

Expectations of debt recovery include an assessment of current expectations of cash flows and their timing, by reference to the carrying value of each debtor's liabilities. Ratings are 1 (High), 2 (Medium) and 3 (Lower).

The following table presents the credit grading for all NAMA-managed debtor connections:

| Debtor performance | A | B | C |

|---|---|---|---|

| Expectation of debt recovery | |||

| 1 | 12% | 16% | 7% |

| 2 | 6% | 12% | 4% |

| 3 | 6% | 16% | 21% |

ENFORCEMENT

An enforcement strategy is pursued by NAMA in circumstances where the debtor's business plan is not considered acceptable, the debtor is in default and is not cooperating or where some other event has occurred that could potentially threaten NAMA's position as a creditor.

By end-December 2012, it had been necessary to make 271 insolvency appointments relating to 207 debtor connections (Table 3).

| Insolvency appointments | NAMA-managed | PI-managed | Total |

|---|---|---|---|

| Corporate | 105 | 111 | 216 |

| Fixed Charge | 27 | 28 | 55 |

| Total | 132 | 139 | 271 |

| Number of debtor connections | 84 | 123 | 207 |

The enforcement process may apply to part of a debtor connection but not necessarily to all of it. Excluding extensions to existing enforcements, there were 61 new appointments made in 2012, 38 of them relating to NAMA-managed connections and 23 to PI-managed connections. By the end of 2012, insolvency practitioners had been discharged in 11 cases as a result of the conclusion of the insolvency process.

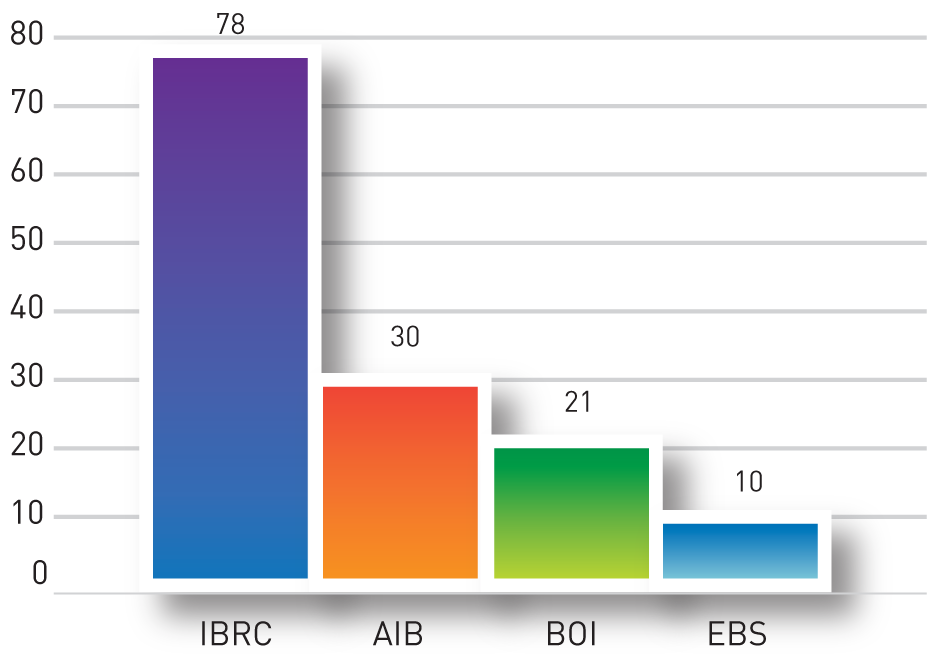

Figure F provides a breakdown of PI insolvency appointments by institution as at end-2012:

| FIGURE F: PI-managed insolvency appointments by institution |

|---|

|

NAMA has introduced measures designed to reduce the level of insolvency fees from those that have applied historically. These measures include utilisation of a mini-tender process for particular appointments, the promotion of the concept of the 'fixed charge receiver' and seeking competitive fixed fee proposals for insolvency assignments.

LOCATION OF BANKRUPTCY PROCEEDINGS

In its position as a secured creditor, NAMA is generally neutral on the locus of bankruptcy proceedings and its experience to date has been that location has not tended to prejudice its recoveries. The Agency has had a positive engagement with the bankruptcy trustees of debtors who have been adjudged bankrupt in the UK. The bankruptcy regime in the UK is well-established and trustees in bankruptcy possess extensive powers to compel the production of legal and banking information on a cross-border basis. These powers have been used in the case of NAMA debtors to uncover significant undeclared assets.

The comparatively shorter duration of bankruptcy in the UK has not been a consideration for NAMA as the bankrupt's unsecured assets remain in the control of the bankruptcy trustee after the discharge from bankruptcy and any failure to make full disclosure can result in the period of bankruptcy being extended beyond the initial one-year period until there is full disclosure.

For a debtor to avail of bankruptcy in any given jurisdiction, he/she must first of all establish that jurisdiction as their Centre of Main Interest ('COMI'). The establishment of COMI is a matter for the relevant authorities in the jurisdiction in which bankruptcy is sought. As at end-December 2012, a total of 48 NAMA debtors had been declared bankrupt: 11 in Ireland and 37 in the UK.

| NAMA Enforced Properties Website Listing |

|---|

| On its website [www.nama.ie], NAMA publishes a listing of properties that are subject to enforcement action. The enforced property details are updated on a monthly basis. At end-December 2012, there were close to 1,600 properties or groups of properties listed on the site. In the majority of cases, the properties are available for sale or are under management and generating income. Since inception, sales by insolvency practitioners have accounted for approximately €1.6 billion of total disposals. Total sales by insolvency practitioners in the 12 months to end-2012 amounted to approximately €557m. In some instances, insolvency practitioners are working through outstanding title defects, ownership, planning and compliance issues with a view to making the properties available for sale as soon as these issues have been satisfactorily resolved. |

| Based on user feedback, the majority of users of NAMA's enforced properties website are interested in properties that are available within their own geographical areas for rent or purchase. NAMA has, in response to feedback from these users, significantly enhanced the functionality of the enforced properties website to enable interested parties to interrogate the listing of properties in a much more informative way. In particular, the enhanced functionality includes the facility to search for properties by property type and county/area and includes links, where applicable, to sales brochures. |

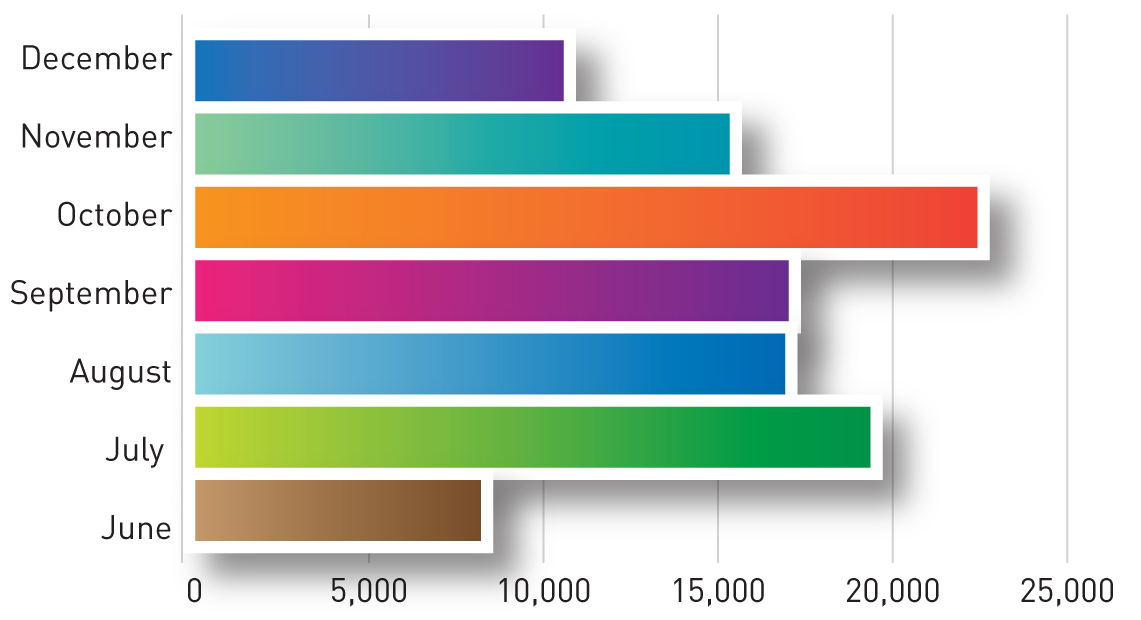

| FIGURE G: User traffic, enforced properties website, June to December 2012 |

|