CHIEF EXECUTIVE'S STATEMENT

In 2012, NAMA entered a new phase. It was the year which marked our evolution from an organisation necessarily focused on setting up its business to one which was addressing that business intensively and comprehensively with the objective of getting the best possible return from it. Having acquired some €74 billion in loans over the course of 2010 and 2011 and having issued debt of close to €32 billion to acquire the loans, it was now necessary for us in 2012 to make progress in terms of repaying that debt. Just over €30 billion of our original debt was in the form of Senior Bonds guaranteed by the Minister and one of the key tasks facing us over time is to remove this contingent liability of the Irish taxpayer. We are confident that we will do so and our confidence is buoyed by the significant progress that we made in 2012 in terms of cashflow generation and debt repayment.

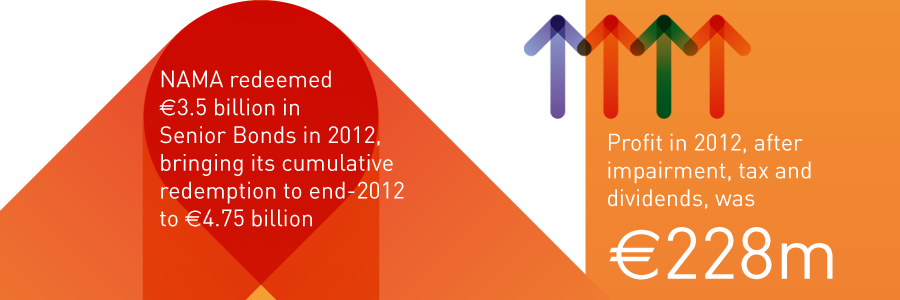

As we see it, the key measure of our capacity to repay our debt is the progress we make in terms of generating cash from our loans. In 2012, NAMA generated €4.5 billion in cash, including €2.8 billion from the proceeds of asset and loan sales by our debtors and receivers. The total cash generated in the three years since our establishment is €10.6 billion. This has enabled us to remain on course to meet our debt reduction targets: by end-2012, we had redeemed €4.75 billion of NAMA Senior Bonds and we are confident that we will meet our end-2013 target of repaying €7.5 billion.

PROPERTY AND LOAN SALES

64% of our cash receipts to date have been generated by property sales by our debtors and receivers and by our loan sales. Almost 80% of those sales to date relate to Britain, reflecting, in particular, the strength and liquidity of the London market and the quality of our assets there. We continue to have a strong exposure to the British market as it accounts for most of the €10 billion of our remaining property collateral which is located outside of Ireland.

We are also selling loan portfolios where this offers the best return. In 2012, we appointed two loan sales advisory panels to assist us in this process and, in the first quarter of 2013, a portfolio of over €800m in loans secured on Irish property was placed on the market through a broker appointed from these panels.

MAXIMISING INCOME

A particular focus for us in Ireland is on maximising non-disposal receipts generated by the assets securing our loans. This has involved, for instance, a major drive to secure tenants for properties which were previously vacant, including thousands of apartments which were empty when we acquired the associated loans. Our portfolio now includes 10,000 apartments which are currently rented, generating an aggregate annual rent of approximately €100m. We are also working hard to increase occupancy and rental income in the context of commercial buildings within our portfolio, including offices and retail properties. The cumulative result of this drive is that we generate about €100m per month in non-disposal receipts across the portfolio, despite the sale in 2012 and earlier years of strong income-producing assets. These receipts are in addition to receipts from asset sales and loan repayments by debtors and receivers. Over the three years to end-2012, we generated about €300m per month on average in cash from disposal and non-disposal receipts.

PROFITABILITY

For the second year in succession, notwithstanding the fact that the Irish property market which secures over half of our loans, suffered further price declines in 2012, I am pleased to be in a position to report a profit. Our operating profit before impairment in 2012 was €826m and, after taking an impairment charge of €518m, we produced a profit before tax of €308m. A tax charge and dividend payments reduced this to a net profit of €228m. Our administration costs fell by 7% to €119m in 2012, mainly reflecting the fact that we are no longer incurring some of the business start-up and due diligence costs which we had to incur in 2011.

Our cumulative impairment charge to date has been €3.3 billion. This largely reflects the fact that our loans were initially valued by reference to property values as at November 2009 and our impairment reviews since then have had to factor in lower expectations for the proceeds from disposal of the Irish assets securing our loans. Thankfully, as the Chairman discusses in his Statement, there was increasing evidence in 2012 to suggest that the Irish market is in the process of stabilising. Notwithstanding our continued prudent approach to impairment, I would expect that in 2013 we will sustain the profitability evident in 2011 and 2012.

WORKING WITH OUR DEBTORS

Achieving the cashflow figures outlined above would have been much more difficult if it were not for the fact that we were able to work constructively with many of our debtors. We are not in the business of gratuitously taking debtors out of business. Our starting point always is to ask whether we can work with them. In assessing that, our key considerations are their commercial viability and competence; in other words, to what extent are they willing and capable of meeting realistic asset management, disposal and debt management milestones? There also has to be a strong element of trust and goodwill: sworn statements of debtor assets and liabilities must be accurate and complete and appropriate cash controls must be in place to ensure that asset income is appropriately funnelled towards debt repayment.

We have reached an accommodation with the majority of our debtors on the basis of undertakings given by them, and, more importantly, of tangible actions taken by them, to work with us to maximise the amounts that can be recovered for the benefit of taxpayers. This includes maximising the security supporting our loans. We now expect to obtain fresh security worth about €750m through a combination of charges on previously unencumbered assets and the reversal of earlier asset transfers by debtors.

At a time when many ordinary borrowers are stretched to the limit in meeting debt repayments, it is only reasonable that the very large debtors who fall within our ambit should be required to apply every asset and every source of income within their control towards repaying their debt. Some of them struggle with this concept and appear to believe themselves worthy of an exalted standard of living which should be financed by others. This cosseted mentality is out of touch with the harsh reality faced by the majority of Irish taxpayers and citizens. Faced with this attitude, we have no alternative but to initiate enforcement after we have exhausted all other feasible options. To date, we have initiated asset recovery proceedings in Ireland, the UK, the US and Canada. We have also referred cases to the Garda Bureau of Fraud Investigation arising from suspected failure by debtors to fully disclose their assets and liabilities.

In addition, we were involved in some high-profile litigation in 2012, including the successful defence of a challenge by Treasury Holdings to the Agency's decision to appoint receivers to certain of its assets and the challenge in the English High Court to the Agency's decision to sell loans associated with the Maybourne Hotel Group, in which the Court ruled in our favour. In all such cases, NAMA's sole concern is to protect and enhance the position of the Irish taxpayer.

PROPERTY MARKET INITIATIVES

The Chairman has referred to the resurgence of international investor interest in Ireland and to the fact that we have an open door to any investors with an interest in acquiring an exposure to the recovery of the Irish property market. This is on the basis that they are willing to deal at realistic, rather than 'fire sale', transaction prices.

We have introduced a number of initiatives which are designed to augment the recovery of the Irish property market and, in particular, to address liquidity constraints. Under our vendor finance initiative which was announced in 2012, we plan to lend up to €2 billion, mainly in Ireland, to purchasers of commercial properties securing our loans. This represents a significant potential injection of liquidity into the Irish market.

In 2012 also, we launched a mortgage initiative designed to facilitate those who wish to buy a home but are concerned about possible future falls in house prices. The 80/20 Deferred Payment Initiative ('DPI') has been well received by prospective buyers. By the end of 2012, sales had been agreed in respect of over 100 of the 295 houses available. The aggregate value of these sales was in excess of €18m by end-2012 and had reached €28m by March 2013. Based on this positive experience, it is our intention to extend the initiative on a phased basis during 2013.

We also welcome the Government's decision to enact legislation to provide for the establishment of real estate investment trusts ('REITS') in Ireland. As an internationally recognised vehicle for investing in real estate, REITs have the potential to increase liquidity in the Irish market, particularly by attracting sources of foreign investment that might not be interested in direct investment in Irish property. Over the longer-run, REITs can also help to professionalise the domestic property sector which traditionally has been too fragmented.

It may take some time for the Irish market to adapt to REITs and to understand how best to optimise their potential but their introduction is a very positive step forward.

The absence of independent, reliable and trusted data on the property market, particularly on likely future trends, is a barrier to efficiency and sustainability in the sector. For this reason, we have agreed to take a lead role in sponsoring new research by the Economic and Social Research Institute ('ESRI'), which will provide the market with unbiased information on the key factors likely to influence the location and cost of housing over a medium-term horizon. These studies will be valuable also to policy makers in areas such as planning and housing who need to be able to prepare well-informed projections as part of their decision-making processes.

CHALLENGES AHEAD

2012 was a challenging year for NAMA staff as we delved deeper into the portfolio and as we reorganised the organisation to reorient ourselves towards asset recovery and asset management. During 2012, 10% of our staff departed as opportunities continue to present themselves elsewhere, not least because of the skills and experience acquired while working for NAMA. While a certain amount of turnover is healthy for any organisation, we also have to be careful that we retain the skillsets required to perform the important work of eliminating the contingent liability of the State by maximising the return on the NAMA portfolio. NAMA is unusual in that all of its staff are employed by the NTMA and assigned to NAMA. The recent announcement of the inclusion of NTMA itself within the remit of public sector remuneration adjustments is certainly a concern in terms of our ability to retain and allocate the correct skillsets to manage the portfolio.

Against this background, I need hardly point out that the absorption and management of the IBRC portfolio will be a major challenge for NAMA. It is my intention that we meet that challenge in a way that does not compromise our capacity to achieve the ambitious debt repayment targets that we have set ourselves on the original loan portfolio that we acquired in 2010 and 2011. For that reason, we will ensure that there is segregation in the management and reporting of the two portfolios. Either portfolio in its own right would be formidable; taken together, the task facing us is very challenging.

CONCLUSION

Finally, I would like to express my appreciation for the dedication, effort and hard work of the Chairman, the Board, the Board Committees, the Executive team and, especially, to the staff assigned to NAMA and also to those within the wider NTMA who contributed to NAMA's success.

Our performance on a number of fronts since inception reinforces my confidence that NAMA will deliver on the challenging mandate which was set for us by the Oireachtas in 2009 and on the no less challenging mandate that the Oireachtas has now asked us to assume in 2013.