NAMA Market Activity

NAMA Asset Disposals

Disposals by location

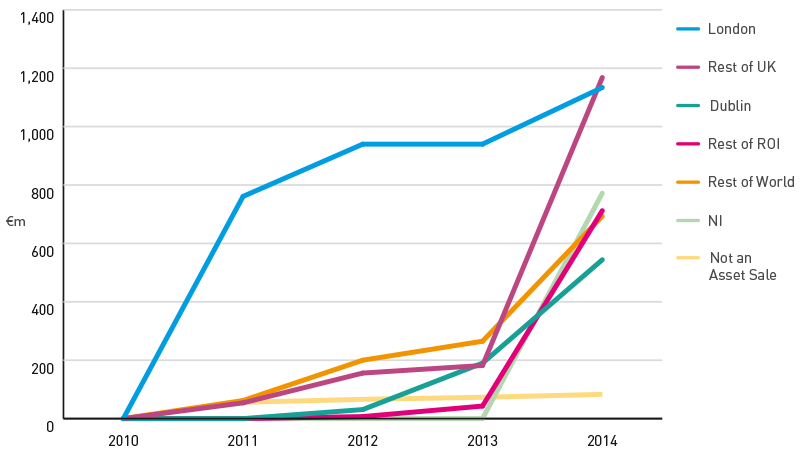

NAMA’s strategy in each of its main markets has been to release assets for sale in a phased and orderly manner consistent with the level of demand, the availability of credit and the absorption capacity of each market. As Figure B illustrates, in the period 2010 to 2013, this meant concentrating sales activity in Britain, particularly London, where commercial investment property yields had fallen in some cases below 3%. Over that period, London assets accounted for 60% of total NAMA disposal proceeds disposal receipts, with assets in the rest of Britain accounting for a further 13%.

Irish assets, by contrast, accounted for just 16% of total disposal receipts in the same period. NAMA strategy was to limit asset disposals into a market where, prior to mid-2013, prices were still trending downwards. NAMA focused primarily during that period in Ireland on ensuring that debtor properties were efficiently managed, that rental and occupancy were optimised and that rental income was fully captured.

Improving conditions in the Irish property market, a desire amongst institutional investors to diversify their real estate risk over wider geographic areas and improving sentiment towards Ireland, enabled NAMA to substantially increase the scale of its disposal activity in the Irish market in 2014 and its overall disposal activity in general. The step change in disposal activity can be seen in total NAMA disposal receipts of €7.8 billion in 2014, an increase of €4.1 billion on total proceeds in 2013. Of the €7.8 billion, 47% or €3.7 billion was generated from the sale of Irish properties and loans. This compares to total Irish disposal receipts in the four years to end-2013 of just over €1.8 billion.

FIGURE B: Disposals by location 2010-2013

FIGURE C: Disposals by location 2014

FIGURE D: Disposals by location since inception

Disposals by sector

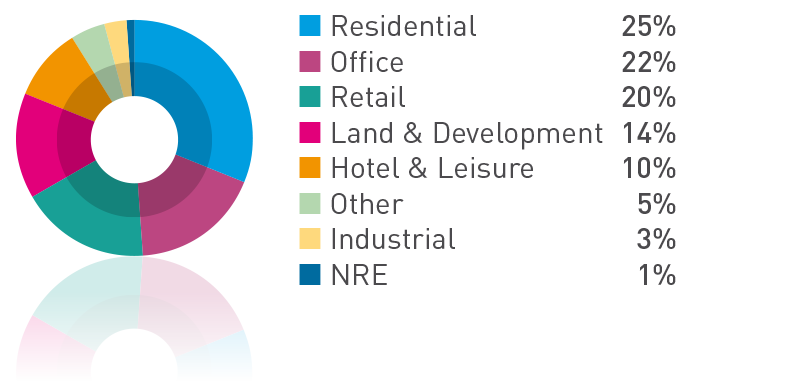

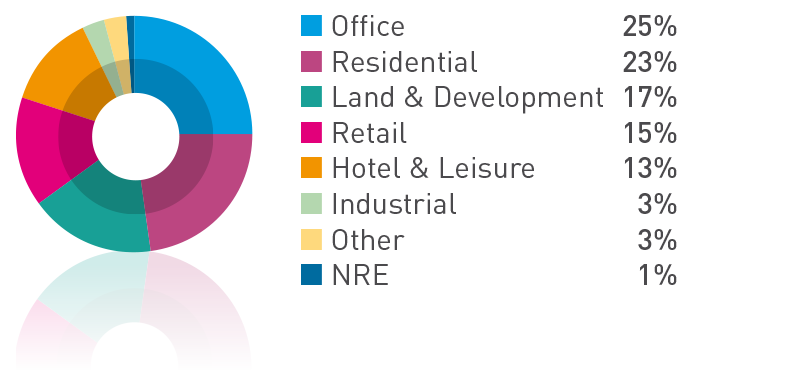

A breakdown of disposals (including loan sales and asset sales) by sector for both 2014 and from inception to end-2014 is shown in Figures E and F. This breakdown underlines the diversity of NAMA’s portfolio with three sectors (residential, office and retail) each accounting for more than 20% of total disposals proceeds in 2014 and two further sectors each accounting for more than 10% of total proceeds.

FIGURE E: Disposals by sector 2014

FIGURE F: Disposals by sector since inception

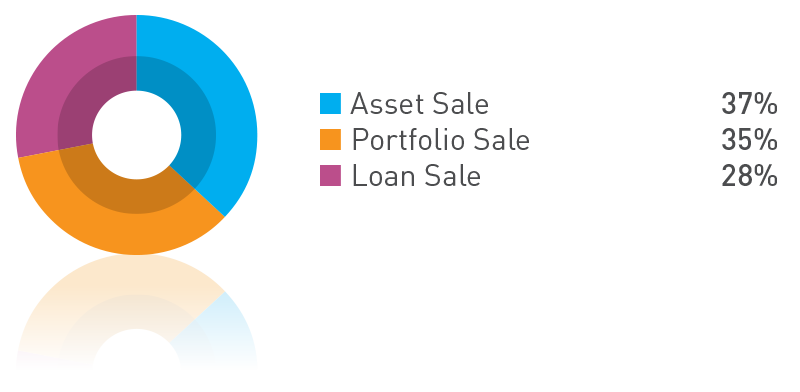

Disposals by transaction type

A key feature of market demand in 2014 was the upsurge in institutional investor interest in multi-asset property portfolios and loan portfolios. This was driven in the main by the effects of monetary easing in the US, by the low level of bond yields worldwide and the relative attractiveness of Irish property yields. Reflecting this, property portfolio and loan portfolio sales have become an increasingly important part of the overall NAMA sales mix, accounting for 63% of Irish disposals in 2014 and 59% of total NAMA disposals in 2014. From inception to end-2014, property portfolio and loan sales accounted for nearly half of all Irish disposals and one-third of disposals across NAMA’s entire portfolio.

NAMA’s market engagements indicate that demand and interest remain strong for portfolio sales with new investors continuing to enter the market and existing investors extending their exposure. This is expected to ensure competitive pricing in 2015 as overseas investors continue to seek opportunities to capitalise on the emerging recovery in Irish commercial property markets at a time when many other asset classes are becoming less attractive.

As Table 2 illustrates, the sale of individual properties is also an important part of NAMA’s overall sales activity. From inception to end-2014, NAMA had overseen almost 7,500 individual disposal transactions involving almost 31,000 individual property units.

TABLE 2: Transactions and property unit disposals 2010 - 2014

| Transactions | No. of Units | |

|---|---|---|

| 2010 | 391 | 583 |

| 2011 | 1,167 | 2,707 |

| 2012 | 1,216 | 4,373 |

| 2013 | 1,859 | 5,172 |

| 2014 | 2,820 | 17,913 |

| 7,453 | 30,748 |

FIGURE G: Disposals by transaction type 2014

FIGURE H: Disposals by transaction type since inception

FIGURE I: ROI Disposals by transaction type 2014

FIGURE J: Selected portfolio sales

Completed August 2014

- Dublin office collection comprising approx. 322,000 sq. ft.

- Approx. €8.5m of secure rental income with 93% occupancy

- WAULT*in excess of 10.7 years

- Strong tenant line up

Completed September 2014

- Approx. 720,000 sq. ft. of retail space and 130 tenants

- Over €13.25m per annum passing rent

- 9.75% approx. initial yield

- Over 70% of portfolio income from institutional grade tenants with a WAULT* of almost 11 years

Completed October 2014

- 761 modern apartments and 34,301 sq. ft. of commercial accommodation

- Gross passing rent approx. €10.4m per annum

- Four development sites extending to approx. 0.70 ha (1.74 ac)

- A further 187 apartments and approx. 85,863 sq. ft. of commercial space being developed

Completed November 2014

- 773,769 sq. ft. of retail space

- Mix of national and international tenant

- Passing rent of approx. €9.5m per annum

- 30 acres of land is available for development

- Overall portfolio WAULT* of 11.09 years

Completing Q2 2015

- Approx. 356,000 sq. ft. collection of five prime Dublin office buildings

- 4 & 5 Grand Canal Square – Two buildings designed by Daniel Libeskind

- One Grand Parade – High profile modern office building

- Alexandra House – 6 storey detached office building with opportunity to refurbish

- 86-88 Leeson Street Lower – 1970s office building in prime Dublin 2 location with planning permission to extend to provide high quality modern space

Significant Property Portfolio Sales in 2014

To help sustain positive momentum in the Irish market and provide investors with certainty as to transaction flow, NAMA signalled at the start of 2014 that it would offer for sale property portfolios in Ireland with a minimum value of €250m in each quarter. The extent of recovery in the Irish market during 2014 meant that the €250m minimum value was exceeded in each quarter. Reflecting this, NAMA approved the sale of a number of very substantial property portfolios with an aggregate market value in excess of €1 billion in Ireland in 2014, including:

| Portfolio | Sector |

|---|---|

| Platinum | Office |

| Central Park | Office/Residential |

| Redwood | Office |

| Acorn | Retail |

| Orange | Residential |

| Parks | Retail |

NAMA brought to the market in 2014 an additional €500m worth of portfolios which will complete in 2015:

| Portfolio | Sector |

|---|---|

| Rockbrook | Residential |

| Plum | Residential |

| Tara | Office |

| Harvest | Retail |

More than 80% of NAMA portfolio sales in Ireland from inception to end-2014 related to Dublin, mirroring both the dominant location of NAMA’s Irish assets and the current focus of investor interest.

FIGURE K: Irish portfolio sales by location since inception

Significant Loan Sales in 2014

FIGURE L: Cumulative loan sale trend since inception by location

In the four years to end-2013, NAMA had completed sales of loans with nominal balances of €3.9 billion. By end-2014 that figure had increased to €13.3 billion, reflecting increased investor interest in larger transaction sizes and the maturing of Europe’s loan sales market.

Some of the major loan portfolio sales which NAMA completed in 2014 are outlined below:

Project Tower

A €1.8 billion par debt portfolio secured on UK student accommodation, UK commercial and development property, Irish development land and Irish retail and residential property, which was sold to an affiliate of the Blackstone Group L.P in Q2 2014.

Project Eagle

A £4.6 billion par debt portfolio, consisting of loans advanced to Northern Ireland based debtors secured primarily by assets in Northern Ireland, Britain and Ireland, was sold to an affiliate of Cerberus Capital Management L.P. in Q2 2014.

Project Drive

A €226m par debt portfolio secured primarily on Irish retail and industrial assets, which was sold to Patron Capital in Q2 2014.

Project Spring

A €438m par debt portfolio secured primarily on Irish office assets, which was sold to Deutsche Bank AG in Q3 2014.

Property Portfolio and Loan Sales Processes

NAMA’s policy is that the sale of all loans and the sale of properties by debtors and receivers should be openly marketed to ensure that the best price available in the market is achieved in all instances. NAMA enjoys a strong reputation in the market for the quality of information it provides as part of its property portfolio and loan sale processes and for the transparent and professional manner in which such transactions have been completed to date. Both its property portfolio and loan sales processes are built on international best practice and NAMA uses experienced advisers to ensure that transactions are executed to the highest market standards and that bidders are treated equally by mapping out a clear and rigorous process to be followed in each sale.

Prior to the launch of a property portfolio or a loan sale, all relevant data, including loan agreements, security and title documentation, data tapes, lease information and tenancy schedules, is assembled in a data room by NAMA in conjunction with its legal and sales advisors. An initial high-level summary of the property or loan portfolio is then issued to potential purchasers so as to generate as much interest as possible.

All potential investors must sign a Non-Disclosure Agreement (NDA) prior to gaining access to each portfolio or loan sale data room. Once the NDA is signed interested parties are legally bound not to have any further contact or share data room information.

Bidders are required to submit binding unconditional bids, proof of funding and marked-up contracts for sale. The final bids are assessed by NAMA with advice and recommendations from the portfolio sales agents or loan sales brokers, and a recommendation is made to the appropriate decision-making authority in NAMA. The successful and unsuccessful parties are advised of the outcome with the successful party also being notified of the timescale for completing the transaction.

A key consideration for NAMA is the mitigation of execution risk. NAMA, in line with standard industry practice in any property portfolio or loan sales process, will not accept conditional bids including bids that are contingent on funding.

To do so would expose NAMA to unnecessary execution risk and damage the credibility of the NAMA sales process and, by extension, the willingness of future prospective bidders to engage in such sales.

Market Trends

The European commercial real estate market experienced record levels of activity in 2014 as investors continued to view the returns offered by property as being attractively priced relative to other investment alternatives such as government bonds or bank deposits. Ireland attracted a very significant portion of this investor activity (an estimated 28%) in what was an unprecedented year for the Irish market. During 2014, it is estimated that over €14.5 billion of Irish assets traded in total, comprising of €4.5 billion of investment property sales and a further €10 billion (traded value) of Irish property loan sales. To put this in context, the previous peak for investment in the Irish property market was approximately €3.5 billion in 2006.

It is also worth noting that since the property crash in 2008-2012 the Irish investment market has transformed from a highly leveraged debt-funded model to an equity-based model, which should put the market on a more sustainable footing and bring it into line with general international best practice.

As the Irish property market continued to move through the recovery cycle in 2014, improving fundamentals across occupational markets replaced pricing as the key attraction for investors. Indeed, stronger pricing was evident across all prime markets as rents increased and yields contracted. Furthermore, there was evidence that as investors looked to move up the risk curve, price recovery slowly started to percolate out to secondary properties and prime regional locations. Also, given the supply-demand imbalances that exist in key segments of the occupier market, most notably Dublin prime office and residential property, a return to development activity became an emerging feature of the market.

Whilst US private equity continued to be the dominant source of investment in the market, a broadening of the investor pool was clearly evident in 2014 as the Irish Real Estate Investment Trusts ('REITs'), domestic institutions and European investors began to participate in the market, thereby adding to the level of competitive tension in asset sales bidding.

A distinguishing feature of the property market over the past two years has been the practice of pooling together assets, in the form of property portfolio sales and loan sales, in order to achieve transactions of sufficient scale to attract large investors. For NAMA, this has proven to be a very efficient and effective mechanism for capitalising on investor demand.

These market dynamics are underpinning the commercial feasibility of new development in Ireland and NAMA is currently providing substantial funding and is facilitating the delivery of new office and residential supply on a commercial basis in Ireland. This is covered in more detail in the Development Funding section of this report.