Debtor Engagement

LOANS ACQUIRED

BORROWING ENTITIES

DEBTOR CONNECTIONS

INDIVIDUAL PROPERTIES

- NAMA acquired more than 12,000 loans linked to 5,000 borrowing entities (managed initially as 780 debtor connections). The loans

were secured by 60,000 individual properties.

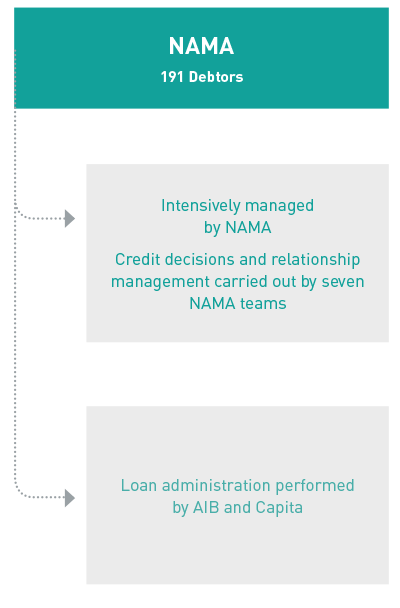

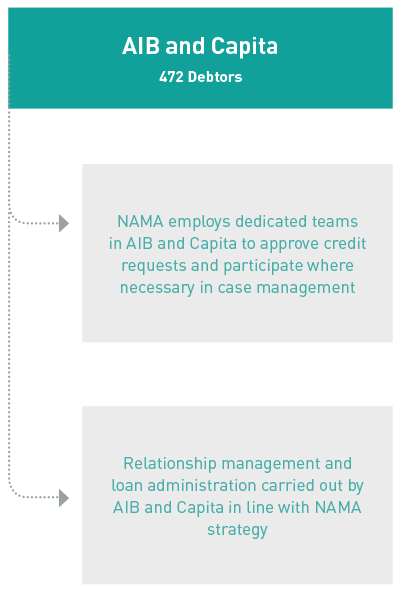

- Following the acquisition of the loans, NAMA directly managed the engagement with the largest debtor connections (referred to as NAMA-managed) and delegated the day-to-day management, within specific delegated authority limits, of smaller debtor connections to the Participating Institutions ('PIs') and Service Provider ('SP') (referred to as PI/SP-managed).

- All debtor business plans were assessed by mid-2012 and strategies approved.

FIGURE A: Day-to-day debtor management

- At end-2014, 663 debtor connections remain: 191 NAMA-managed and 472 PI /SP-managed.

- By value, NAMA is in a consensual workout with debtors who account for 70% of its loan portfolio. A consensual workout means that debtors manage the agreed property and realisation strategy, under close monitoring by NAMA. Consensual workout arrangements may include some or all of the following:

– Schedules of agreed asset or loan sales.

– Reversal of certain asset transfers.

– Charges over unencumbered assets.

– NAMA has obtained charges over additional security, through both the reversal of asset transfers and charges over unencumbered assets, with combined value of more than €800m.

– Rental income from investment assets controlled by debtors have been brought within NAMA’s control with rents lodged to bank accounts over which NAMA has security.

– NAMA provides funding for viable commercial and residential development projects with a view to increasing the longer-term recoverable value of assets.

- During the period from 2010 to 2012, NAMA agreed business plans with the majority of its debtors. NAMA disclosed in

its 2010 Annual Report (published in July 2011) that asset management and incentivisation mechanisms could be a feature if better-than-expected financial outcomes were achieved by debtors.

The outcome of the review of some debtors’ business plans included asset management and incentivisation mechanisms which would only be triggered if they met very ambitious or ‘stretch’ financial targets which were set for them. In certain cases, if debtors achieve these stretch targets, they may retain a proportion of any excess achieved above target levels. The major share of any excess will go to NAMA and ultimately to taxpayers if the stretch financial targets are achieved. Had such fee arrangements not been agreed with debtors, it is very probable that the consequences would have been a significantly reduced return in terms of the disposal value of assets and in the ultimate return to NAMA and to taxpayers.

The objective of these mechanisms was to ensure that debtors were motivated to extract maximum value from the workout and realisation of their assets. At this stage, NAMA expects that very few debtors will achieve the stretch financial targets set for them. However, the continued strong improvement in property market conditions since the end of 2013 has triggered asset management fee payments in a small number of cases. The major part of the benefit of the strong financial outcomes likely to be achieved by these debtors will flow to NAMA and to taxpayers.

- To date there have been 456 insolvency appointments across 353 debtor connections who account for 30% of NAMA’s loan portfolio by value (Table 1).

TABLE 1: Enforcements as at end-December 2014

| Insolvency Appointments | NAMA Managed |

PI/SP Managed |

Total |

|---|---|---|---|

| Corporate | 138 | 218 | 356 |

| Fixed Charge | 43 | 57 | 100 |

| Total | 181 | 275 | 456 |

| Number of Debtor Connections | 108 | 245 | 353 |